Investors are returning to the London nickel market with hefty bets that prices will fall, in a trend could set the stage for a fresh bout of volatility after steep declines this year.

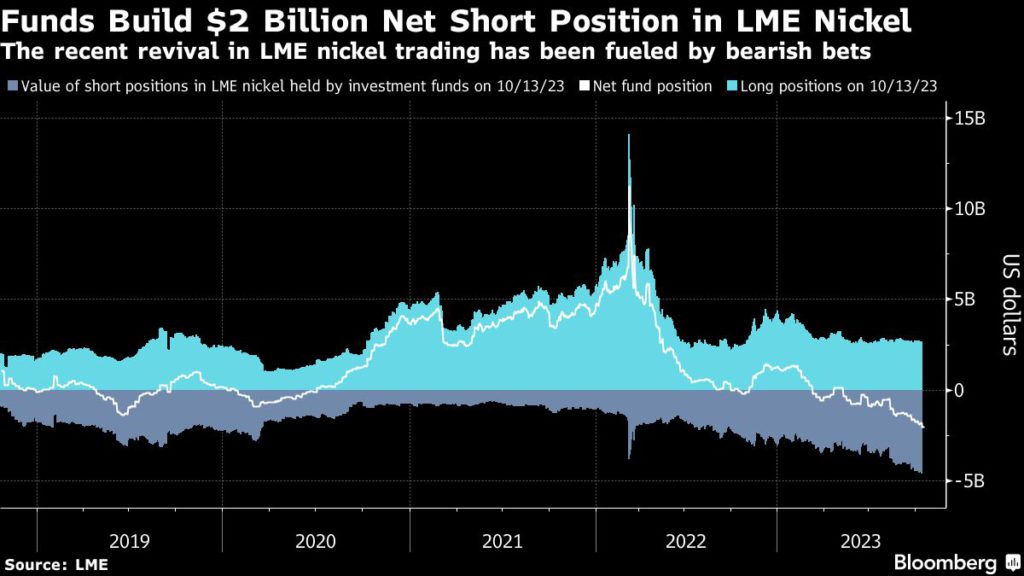

Funds have amassed $4.6 billion in short positions against London Metal Exchange nickel contracts, helping to create a net short position valued at $2 billion, according to data from the bourse. Measured by value, that’s a record in data going back to 2018, while in tonnage terms the mismatch is near an all-time high seen in 2019.

The influx has helped to revive the beleaguered nickel market, after trading plunged dramatically last year in the wake of the LME’s controversial decision to cancel $12 billion in trades to rein in a runaway short squeeze.

After more than a year of illiquid trading, the LME has celebrated the recent upturn in activity, with chief executive Matthew Chamberlain earlier this month expressing cautious optimism that the market is stabilizing. But the growing mismatch between bulls and bears also risks stoking volatility again, and if positioning becomes more extreme it could serve as an acid test for trading controls the LME introduced after the crisis.

Prices were whipsawing last week, with brief rallies that some brokers attributed to investor short covering being followed by further declines that have brought nickel’s total loss for the year to about 38%. But so far, there are no signs that the erratic trading conditions that have dogged the contract until recently are creeping back in.

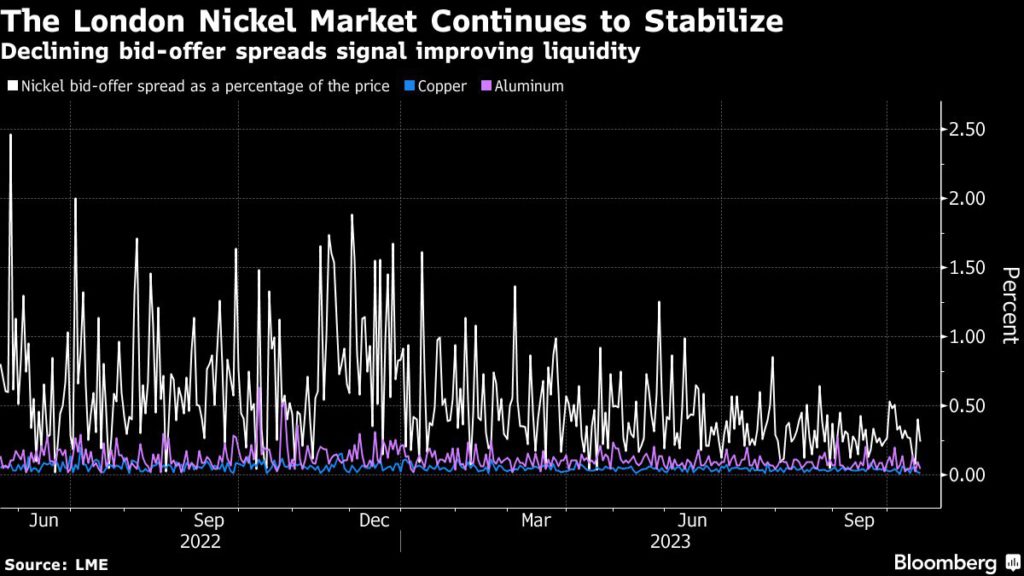

Intraday price swings have been modest, and the spread between bids and offers at the close of trading has continued to decline, moving closer to levels seen in the more liquid copper and aluminum markets. Even if there is a haphazard rush to unwind bearish positions, the most prices could move in any given day is 15% — meaning that a repeat of last year’s 250% rally in a little over day is impossible.

In the nickel crisis, the surge in prices started as the invasion of Ukraine sparked fears over supply from Russia, providing a fundamental pretext for funds to build up long positions.

Simultaneously, banks rushed to cover losses on huge bearish off-exchange bets held by some physical producers, particularly China’s Tsingshan Holding Group Co. Brokers also scrambled to unwind short positions held on the LME, causing a spike in prices and billions of dollars in margin calls that the LME said would have sent the market into a “death spiral” if it hadn’t intervened.

One irony of Tsingshan’s disastrous wrong-way bet that prices would fall as supply rose is that — after effectively being bailed out by the LME — the company has ultimately been proven right. A wave of new supply brought on by Tsingshan and others in Indonesia is pushing the market into a yawning surplus, and there are widespread expectations that more and more of it will start finding its way into the LME’s warehousing network.

The gloomy fundamental backdrop meant there were few bulls in sight at an annual gathering of the metals world in London last week, and bearish investors may feel emboldened to double down on their positions if nickel does start flooding in.

But with nickel prices trading near two-year lows around $18,600 a ton, producers outside of Indonesia are increasingly feeling the strain. Glencore Plc, for instance, has said it will stop funding its struggling Koniambo Nickel mine in February, putting its future in doubt after years of losses.

Before last year’s short squeeze brought infamy to the nickel market, it already had a well-earned reputation as the most volatile metal on the LME. That was largely due to its frequent extreme reactions to rumored shifts in supply and demand. If the nickel market really is getting back to its old self, bearish investors may do well to keep one eye on the exit.

(By Mark Burton)