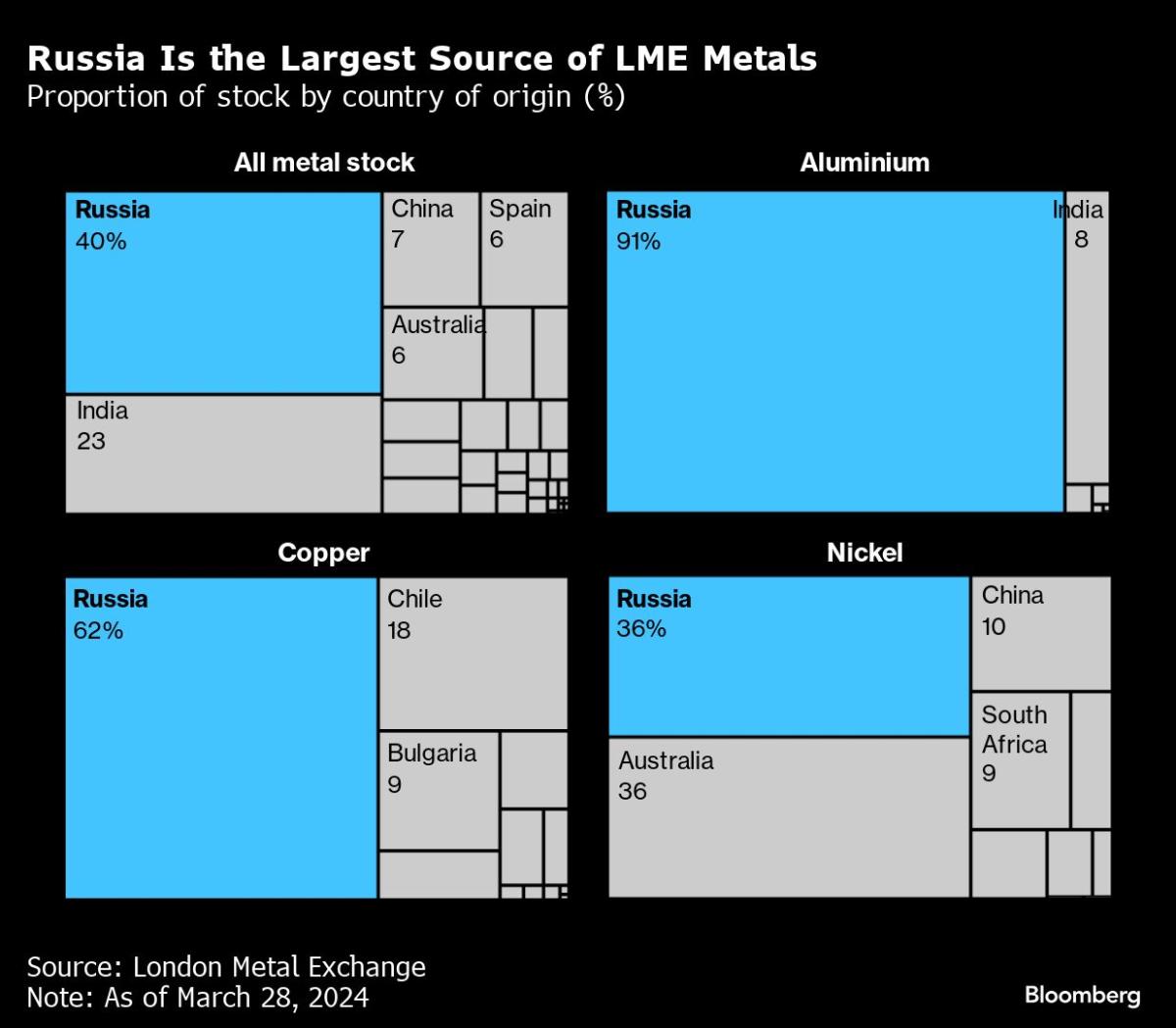

The Biden administration has unveiled plans to exclude Chinese entities from receiving any of the generous tax credits available for investing in the US electric vehicle (EV) supply chain.

Both the Bipartisan Infrastructure Law, which allocated $6bn of credits for batteries and the critical minerals required to make them, and the Inflation Reduction Act (IRA), which includes a subsidy of up to $7,500 for each new energy vehicle, explicitly exclude any “Foreign Entity Of Concern” (FEOC).

That term hadn’t been defined until Friday, when the Department of Energy and US Treasury confirmed it would apply to China, Russia, North Korea and Iran.

The administration is also proposing tough criteria, including a 25% ownership threshold, for determining whether a company is controlled by a FEOC.

Given China’s dominant position in the global battery supply chain, often in the form of joint ventures with Western partners, the new rules could have far-reaching consequences for critical mineral producers just about everywhere.

Time-line tensions

The proposed FEOC rules, which are open to a 30-day consultation, mean that from next year no clean-energy vehicle can qualify for a subsidy if it contains any battery components that are manufactured or assembled by a FEOC.

Beginning in 2025, the restrictions will widen to include any critical minerals in the battery that are extracted, processed or recycled by a FEOC.

There is some wriggle-room granted for “non-traceable battery materials” in electrolyte salts, electrode binders and electrolyte additives. These, typically accounting for less than 2% of the value of critical minerals in the battery, will be exempt until 2027.

That delayed time-line has infuriated Senator Joe Manchin, the original architect of the linkage between EV subsidy and mineral sourcing in the IRA. He promised to “take every avenue and opportunity to reverse this unlawful, shameful proposed rule.”

However, the simple fact is that, to quote Treasury, “industry tracing of these particular applicable critical mineral production processes is uncommon and third-party standards for doing so are underdeveloped.”

If such materials weren’t exempted, “no car models might have qualified for tax credits next year,” according to John Bozzella, head of US automotive trade group the Alliance for Automotive Innovation.

Shifting the supply chain

The FEOC rules are intended to dovetail with the IRA’s requirement that any EV subsidy is contingent on a percentage of all material inputs being sourced either domestically or from a Free Trade Agreement (FTA) partner. The percentage threshold rises from 30% this year to 80% in 2027.

The aim is clearly to incentivize the build-out of a domestic mine-to-battery supply chain and simultaneously wean US automakers off their dependence on China.

But it poses significant problems for both countries and companies that have partnered with Chinese entities for the supply of battery inputs such as lithium, cobalt and nickel.

Indonesia, for example, has emerged as the world’s largest nickel producer in recent years.

It does not have a free trade agreement (FTA) with the United States and its request for even limited talks on a critical minerals deal has been shunted into the slow lane.

That’s because Indonesia’s nickel sector is dominated by Chinese players, who have pioneered processing the country’s relatively low-grade nickel deposits into high-purity battery inputs such as nickel sulphate.

As things stand, only a handful of operators such as state-owned Antam and Vale Indonesia could pass the FEOC hurdle in the event Indonesia reached a trade agreement with the United States.

Even many companies operating in an FTA partner country such as Australia are unlikely to qualify for the IRA tax largesse given many are in joint ventures with Chinese players.

The Greenbushes mine, the world’s largest producer of lithium concentrates, is 26% owned by Chinese-owned Tianqi Lithium, while the Mt Marion lithium mine is 50% owned by China’s Ganfeng Lithium, according to analysts at Project Blue.

Even a mine that has no Chinese ownership won’t qualify for IRA subsidies if the raw material is processed at a Chinese or Chinese-controlled processing plant.

Ripple effects

China currently accounts for almost two-thirds of the world’s lithium processing capacity, 75% of its cobalt capacity, 95% of its manganese capacity and just about all of its graphite capacity.

It is, however, short of mined raw materials and has locked in future supply via equity holdings in each metallic stream of the battery chain.

The country’s overseas partners may now have to think long and hard if they don’t want to be excluded from the US market for new energy vehicles.

There is likely to be much reshuffling of corporate structures, although that may not be enough to pass the Department of Energy’s “effective control” test.

“Effective control” is interpreted to mean a FEOC using technology licensing or contractual off-take terms to control an entity’s production and processing.

There is also likely to be much investment in new Western capacity that is not tied to China.

That is of course the whole purpose of the IRA-FEOC package but in the short term there may be more losers than winners in the global battery supply chain.

(The opinions expressed here are those of the author, Andy Home, a columnist for Reuters.)

(Editing by Sharon Singleton)