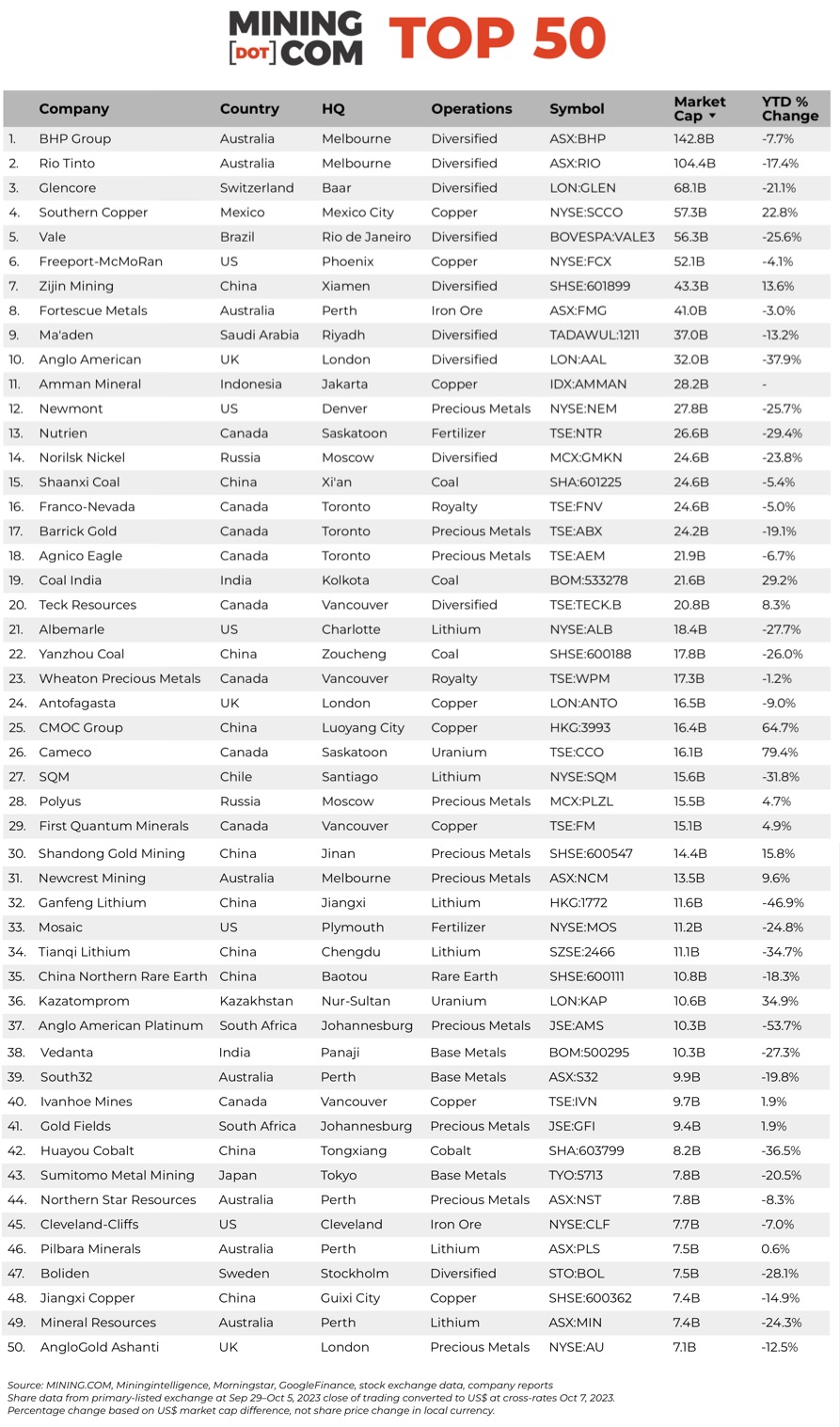

Amid a wider slump ranking of world’s biggest miners were lit up by newcomer Amman Minerals which now sits just outside the top 10 after minting at least six new billionaires since its July IPO.

At the end of Q1 2022, the MINING.COM TOP 50* ranking of the world’s biggest miners hit an all-time record of a collective $1.75 trillion as copper spent time above $10,000 a tonne, real nickel trades were being made above $40,000, lithium shipped for over $60,000 and everything from gold and platinum to uranium and tin were rallying hard.

Uranium prices have doubled since then to above $60 a pound, tin is also trading higher although well below its March 2022 peak while gold’s recent safe haven rally means the precious metal is also trading higher compared to March 2021.

Iron ore, where the top diversified mining companies dig for most of their profits, has also held up remarkably well trading at $120 a tonne this week, little changed from end-June.

Base and battery metals however have entered a deep slump since those heady days. Copper, zinc and aluminium are firmly in bear market territory down by a fifth a more, nickel and palladium investors are nursing 40%+ losses, cobalt is nearing record lows and lithium prices are hovering above $20,000.

After defying weakness on metals markets due to high expectations of strong future demand, particularly for copper, lithium and nickel, mining stock valuations have now succumbed.

At the end Q3 2023 mining valuations for the industry’s top tier have slumped a total of $516 billion since the all-time highs. Declines so far this year total $145 billion for a combined market value of $1.38 trillion – back to levels seen at the end of September 2021.

Just how bad sentiment is across the board is evident from the best performer list for Q3, which includes for the first time three counters which lost ground over the period.

Archipelago ascent

The first Indonesian company to make it into MINING.COM’s ranking of world’s 50 most valuable mining companies, Amman Minerals Internasional, has surged 213% in US dollar terms since its July debut in Jakarta to reach a market capitalisation just shy of 450 trillion rupiah or more than $28 billion.

Amman Minerals is the owner and operator of the giant Batu Hijau copper and gold mine in production since the turn of the millennium and is developing the adjacent Elang project on the island of Sumbawa.

Elang is one of the world’s largest undeveloped copper and gold porphyry deposits and is currently in the feasibility stage. Elang boasts 4.7 million tonnes of proven and probable copper reserves and over 15 million ounces of gold.

Indonesia has become a red-hot IPO market this year and Amman was the largest of the year so far raising more than $700m in its IPO, and now sits at number 11 on the ranking.

Bloomberg reports Amman Minerals’ ascent has minted at least six new billionaires including chairman Agus Projosasmito whose stake in the company is now worth $2.7 billion. The miner’s spectacular market performance has also added $4 billion to the net worth of Anthoni Salim, who helms one Indonesia’s largest conglomerates, taking the tycoon’s paper billions to within shouting distance of double digits.

Indonesia’s other major mining IPO, Harita Nickel, is on a different trajectory altogether. Listed on the Indonesian Stock Exchange in April raising $672m, the company has had a tough go of it and the stock has shed more than 60% since then as nickel prices continue to decline.

Lithium losses

The strength of the lithium sector outside China had been remarkable given the precipitous decline in prices for the battery metal since hitting all time highs above $80,000 a tonne in November last year.

But during Q3 the slump in prices of the battery raw material caught up with the six stocks represented in the Top 50, for a combined loss of over $30 billion in market cap over the three month period to just over $70 billion.

Measured from their 52-week highs the correction in the sector has been brutal – Perth-based Pilbara Mineral has bled 31% in market cap making it the best performer. Mineral Resources has given up 37% while the declines for Albemarle, SQM, Ganfeng and Tianqi have been over 50%.

Pilbara Minerals, which unlike its peers is clinging onto year-to-date gains, joined the Top 50 last quarter and brought the number of companies based in the Western Australia capital to five, surpassing the tally of Vancouver, BC as the top home base in the ranking.

The chances of another Perth-based lithium miner, IGO, of entering the Top 50 has dimmed. With a market cap of $5.4 billion, the company is down to the mid-60s in the ranking.

The merger of US-based Livent and Australia-Argentina lithium miner Allkem, expected to close before 2023 is out, may also not be enough to enter the Top 50. Together the two companies are now worth $7.4 billion, which would edge out AngloGold Ashanti for the last spot, but the fortunes of lithium and gold going into 2024 are diverging widely.

Enriched uranium

In September, uranium scaled $60 per pound for the first time since 2011. The breakthrough for the nuclear fuel comes after a decade in the doldrums following the Fukushima disaster in Japan.

The World Nuclear Association predicts world reactor requirements for uranium to surge to almost 130,000 tonnes (~285 million pounds) in 2040. That’s up from an estimate of 65,650 tonnes in 2023.

A significant portion of the WNA’s upward growth adjustments can be attributed to the accelerated adoption of Small Modular Reactors or SMRs as part of decarbonisation efforts for a range of industries from shipping to data centres with powering remote mine sites near the top of the list for SMR potential.

Canada’s Cameco makes the best performer list over the three months again in Q3 after spending much of the post-Fukushima period in the wilderness. The Saskatoon-based company enters the top 30 for the first time after jumping 19 places so far this year.

The value of shares in Kazatomprom, the world number one uranium producer, topped $10 billion at the end of Q3 placing it at position 36. Until this year the state-owned Kazakh company was outside earshot of the Top 50 since its dual-listing in London and Astana in 2018.

Diversified drop

BHP’s market position has also been supported by uranium prices as the Melbourne-based company boosts output at its Olympic Dam operations.

The world’s top mining company’s market value has declined by less than 8% year to date for a $142 valuation , outperforming other diversified heavyweights Rio Tinto, down 17%, Glencore (–21%), Vale (–25%) and Anglo American (–38%).

London-listed Anglo American, has had a rough year in part due to its exposure to platinum group metals and control of Anglo American Platinum, and is now valued at $32 billion after peaking at $70 billion in March 2021.

Investors in Anglo, with a history going back more than a hundred years on the South African gold and diamond fields, have had a particularly wild ride over the last few years. In January 2016, Anglo’s market cap fell below $5 billion after it came close to suffocating under a pile of debt.

The dramatic slump in palladium prices (down 38% this year) and platinum (–16%) have also seen AngloPlat drop to its lowest position ever at a valuation of $10 billion, down from nearly $40 billion end-March 2021.

Former PGM high flyers Impala Platinum and Sibanye Stillwater, both valued around the $4 billion mark today, have lost sight of the Top 50 altogether.

*NOTES:

Source: MINING.COM, Mining Intelligence, Morningstar, GoogleFinance, company reports. Trading data from primary-listed exchange at Sep 29-Oct 5, 2023 where applicable, currency cross-rates Oct 7, 2023.

Percentage change based on US$ market cap difference, not share price change in local currency.

As with any ranking, criteria for inclusion are contentious. We decided to exclude unlisted and state-owned enterprises at the outset due to a lack of information. That, of course, excludes giants like Chile’s Codelco, Uzbekistan’s Navoi Mining, which owns the world’s largest gold mine, Eurochem, a major potash firm, and a number of entities in China and developing countries around the world.

Another central criterion was the depth of involvement in the industry before an enterprise can rightfully be called a mining company.

For instance, should smelter companies or commodity traders that own minority stakes in mining assets be included, especially if these investments have no operational component or warrant a seat on the board?

This is a common structure in Asia and excluding these types of companies removed well-known names like Japan’s Marubeni and Mitsui, Korea Zinc and Chile’s Copec.

Levels of operational or strategic involvement and size of shareholding were other central considerations. Do streaming and royalty companies that receive metals from mining operations without shareholding qualify or are they just specialised financing vehicles? We included Franco Nevada, Royal Gold and Wheaton Precious Metals on the basis of their deep involvement in the industry.

Vertically integrated concerns like Alcoa and energy companies such as Shenhua Energy where power, ports and railways make up a large portion of revenues pose a problem as does battery makers like CATL which is increasingly moving upstream, but where mining still make up a small portion of its valuation.

Another consideration is diversified companies such as Anglo American with separately listed majority-owned subsidiaries. We’ve included Angloplat in the ranking but excluded Kumba Iron Ore in which Anglo has a 70% stake to avoid double counting. Similarly we excluded Hindustan Zinc which is listed separately but majority owned by Vedanta.

Many steelmakers own and often operate iron ore and other metal mines, but in the interest of balance and diversity we excluded the steel industry, and with that many companies that have substantial mining assets including giants like ArcelorMittal, Magnitogorsk, Ternium, Baosteel and many others.

Head office refers to operational headquarters wherever applicable, for example BHP and Rio Tinto are shown as Melbourne, Australia, but Antofagasta is the exception that proves the rule. We consider the company’s HQ to be in London, where it has been listed since the late 1800s.

Please let us know of any errors, omissions, deletions or additions to the ranking or suggest a different methodology.