- Rio exported 331.8Mt of iron ore from the Pilbara in 2023, its second highest production year on record

- No major surprises in first major quarterly of 2024

- Ravensthorpe nickel scaled back as sector woes continue

No alarms and no surprises in the Rio Tinto (ASX:RIO) numbers today, revealing the world’s biggest iron ore exporter shipped 331.8Mt of the red dirt out of the Pilbara in 2023.

That came in towards the upper end of guidance, with costs expected to be in the lower half of Rio’s range of US$21-22.5/t.

After lifting output by 3% this year, Rio has already revealed it could incrementally lift production in 2024 if it hits the upper end of its guidance range of 323-338Mt.

But it will still be using elevated levels of its cheapie product — SP10 — to do that with only the development of a string of replacement mines and the higher grade Rhodes Ridge orebody by the end of this decade expected to ensure the bulk of its product mix is the benchmark Pilbara Blend product.

That will come after the development of the Simandou mine in Guinea, which Rio late last year revealed would cost it US$6.2b for its share of the development.

It is expected the world’s largest undeveloped high grade iron ore deposit will be producing from 2025, with Rio’s share of two of the four blocks to net it 27Mtpa of additional production after a 30-month ramp up to its nameplate capacity of 60Mtpa.

Rio also enjoyed a 17% lift in iron ore prices, with the average monthly price on the 86.3Mt it shipped from the Pilbara hitting US$129/t in the fourth quarter.

In its results, Rio noted the challenges posed by recession fears and supply chain risks in the Panama and Suez Canals along with labour costs across Australia, Canada and the USA.

But in its key market, China, it is predicting a ‘gradual recovery’ from the second half of 2024.

“China’s economy stabilised earlier in the fourth quarter. Resilient infrastructure and manufacturing investment, and an increase in the automotive sector and consumer goods, helped offset the prolonged weakness in the property market,” Rio said.

“Market confidence increased following strong fiscal easing and improvement in manufacturing and consumption levels. Stimulus measures are expected to drive a gradual recovery in 2024, albeit weighted towards the second half, with the real estate sector remaining weak.”

Rio’s average iron ore sales price for the second half of 2022 came in at US$109.6/dmt, up from US$107.2/dmt in the first half, with full year sales of US$108.4/dmt up from US$106.1/dmt in 2022.

But pellet prices from its high grade Iron Ore Company of Canada operations in Quebec fell from US$190.3/wmt to US$155/wmt in 2023 as premiums for higher grade products tumbled.

Rio’s figures show exports of SP10 fines jumped a massive 56% YoY in 2023 to 35.4Mt, while Pilbara Blend Fines exports fell 5% to 105.1Mt, though Pilbara Blend Lump product shipments rose 11% to 59.7Mt.

Salt sale, Winu activity and lithium outlook

Rio’s mined copper output meanwhile rose 2% to 620,000t, despite a 6% fall in the fourth quarter to 160,000t, with costs expected to fall in the upper half of its 180-200 US cents range.

Rio plans to up that to 660-720,000t in 2024 with refined copper output rising from 175,000t to 230-260,000t on the completion of a rebuild at the Kennecott Smelter in the US and ramp up at the Oyu Tolgoi mine in Mongolia, where Rio now has a 66% stake alongside the Mongolian Government.

There was some movement in the fourth quarter on the long delayed Winu project, a new copper and gold discovery in WA’s Paterson Province, with Project Planning Agreements executed with the Nyangumarta and Martu traditional owner groups.

Rio says it has now progressed studies, drilling and fieldwork enough to begin its formal EPA approval process, with project agreements with those TO groups among the key priorities.

The $175b giant has also announced the sale of a non-core salt asset in Carnarvon called Lake MacLeod to Leichhardt Industrials Group, netting $375 million for the project which produces 1.5Mt of sale per annum and 1Mtpa of gypsum.

“The sale of Lake MacLeod will enable Dampier Salt to focus on enhancing operational efficiencies at its remaining two Pilbara operations, while allowing the new owner of Lake MacLeod to maximise its potential,” Rio’s MD of port, rail and core services Richard Cohen said.

“Until the completion of the sale, the Dampier Salt leadership team’s focus will be on safety, delivering on plan, and maintaining respect for all people at Lake MacLeod and in the Carnarvon community.

“We are pleased Leichhardt has committed to retaining all Lake MacLeod employees, ensuring continuity of operation and providing job stability to the 130-strong workforce.”

Rio’s 68% owned Dampier Salt JV, co-owned by Japan’s Marubeni Corporation (22%) and Sojitz (10%), produces around 10Mt of salt a year.

Meanwhile, Rio says it remains positive on the long-term outlook for lithium, expecting a 3000tpa starter lithium carbonate plant to be in operation at its Rincon Salar in Argentina by the end of this year.

“The decline in the lithium carbonate spot price continued in the fourth quarter, having fallen ~80% since early 2023, driven by increased global mine supply and destocking along the supply chain,” Rio said.

“Electric vehicle (EV) demand growth slowed, albeit from a higher base.

“Market fundamentals for lithium remain strong over the longer term. EV penetration rates will continue to increase as countries decarbonise and more investment into mine supply will be required to fill the supply gap.”

Rio’s bauxite output was unchanged at 54.6Mt in 2023 after an 8% lift in output in the December quarter on better weather and the end of equipment issues at its Weipa and Gove mines, while aluminium output lifted 9% on the year to 3.3Mt for calendar 2023.

Alumina output came in at 7.5Mt, within its 7.4-7.7Mt guidance range.

RBC’s Tyler Broda and Kaan Peker said there were no major surprises, with only the previously downgraded Kennecott and IOC operations missing their original guidance.

“With iron ore shipments inline we would expect minimal movement to consensus earnings heading into the full year results albeit mined copper was 6% behind cons,” they said in a note.

READ: In pictures: How Rio has made the world’s biggest iron ore business into a machine

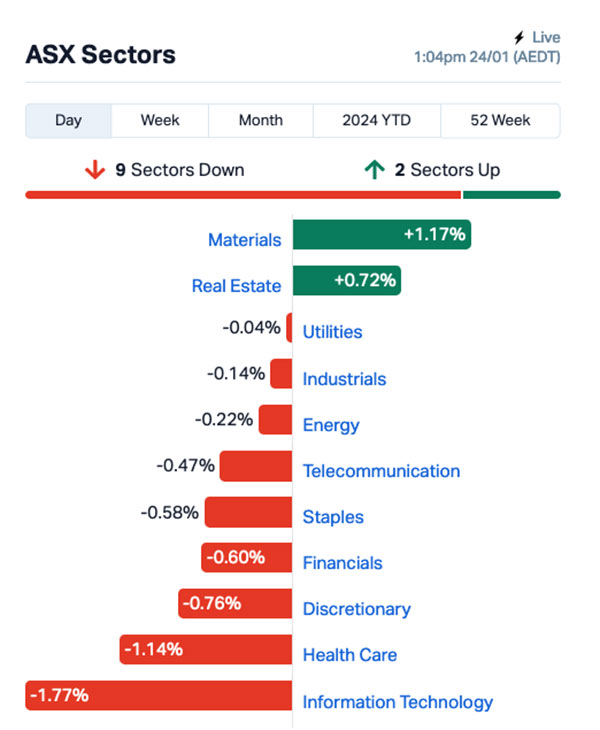

Rio Tinto (ASX:RIO) share price today

Also not a surprise …

Is news of the curtailment of the Ravensthorpe nickel mine in WA where beleaguered TSX base metals producer First Quantum Minerals says it will cut 30% of its 420 strong workforce at the operations.

The decision follows the closures of the mine twice in the past 15 years — first in 2009 under BHP (ASX:BHP), not long after it spent billions building the nickel laterite operations, then under new owner FQM in 2017.

Since its third revival South Korean battery and steelmaker POSCO had entered the fray, paying US$240 million in 2021 for a 30% stake.

It will still sell around 16,000t of nickel annually over the next three years, but only using stockpiled ore that can be processed through atmospheric leaching.

Mining will stop, preserving the higher grade Shoemaker-Levy orebody, with the more expensive high pressure acid leach plant to be halted. It will try to mine the established Halley and Hale-Bopp orebodies as prices recover.

Unlike the sulphide nickel operations mined by companies like BHP, IGO (ASX:IGO) and Mincor (now part of Andrew Forrest’s Wyloo Metals), Ravy is a nickel laterite orebody, generally regarded as costlier to process and extract the nickel from.

Only one other nickel laterite mine is in operation in WA — Glencore’s Murrin Murrin — but it has a lower cost base and higher cobalt content, generating stronger by-product credits.

Indonesia’s dominant nickel industry, whose growth in the past two years has sunk prices from over US$30,000/t to US$16,208/t yesterday, also operates laterite orebodies. But it has brought costs down through Chinese companies’ rollout of novel processing technologies co-located at large industrial parks.

FQM had already lowered production guidance for last year from 23,000-28,000t to 22,000-24,000t at its Q3 results last year and ate all in sustaining costs at Ravensthorpe of between US$11-11.90/lb, against current prices of around US$7.40/lb.

And it’s facing challenges elsewhere, with the Panamanian Government effectively shutting its flagship Cobre Panama copper mine, forcing the company to look for cost savings.

Even WA’s nickel sulphide operations are struggling amid dwindling reserves and rising costs, with IGO last year shutting one of the nickel mines acquired in its disastrous takeover of Western Areas — the full $1.3b value of which could soon be written off.

Panoramic Resources went under late last year, with administrators halting its Savannah nickel mine earlier this month, prompting the loss of 140 jobs.

READ: POSCO just grabbed a slice of Ravensthorpe nickel; here’s why our juniors are smiling

ASX nickel plays share prices today

The post Ground Breakers: Rio Tinto hits upper end of iron ore guidance in day of few surprises appeared first on Stockhead.