- Future Metals releases scoping study for Panton PGM-nickel-chromite project in WA

- Study outlines robust economics for only near-term PGM supply outside of volatile jurisdictions Russia and South Africa

- FME says project can withstand price downturns and leverage upswings

- Pre-feasibility study now underway for completion in Q4 2024

Special Report: Future Metals Panton platinum group metals (PGM) project in WA could be one of few significant primary PGM operations in the western world.

PGMs are crucial to multiple decarbonisation technologies, but supply is heavily concentrated in the volatile jurisdictions of Russia and South Africa.

Panton’s status as the highest grade PGM deposit in Australia, a top tier Western mining jurisdiction, makes it one to watch.

A scoping study released today supports a high-grade, initial 9-year operation processing both reef and high grade dunite material – an important commercial source of PGMs and chromium – through conventional crush, grind, and flotation.

Average annual life of mine production would be 117,000oz PGM 3E (platinum plus palladium and gold), 134,000t chromite concentrate and 1,200t of nickel (161,000oz palladium equivalent) – making it “one of few significant primary PGM operations in the western world”.

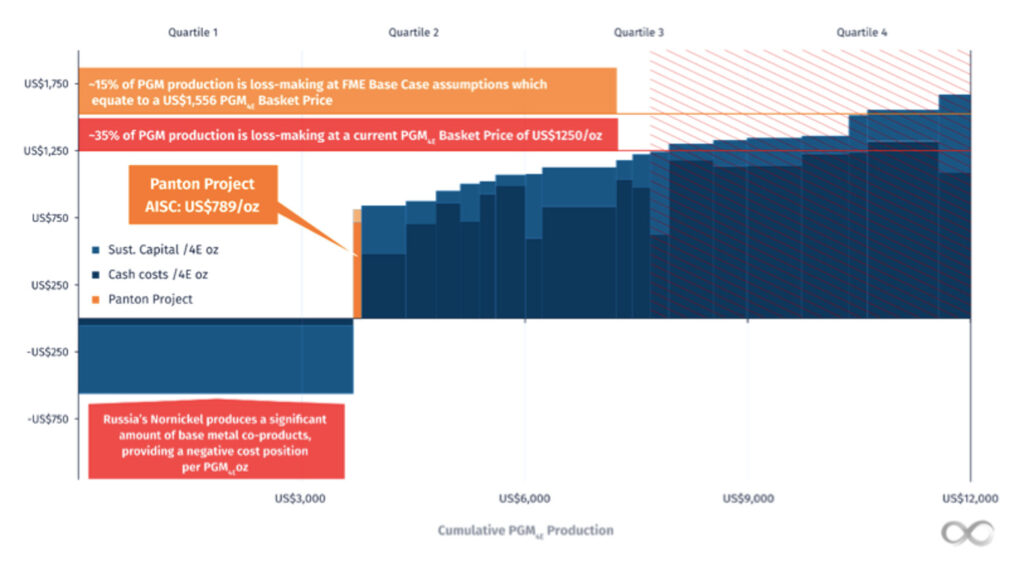

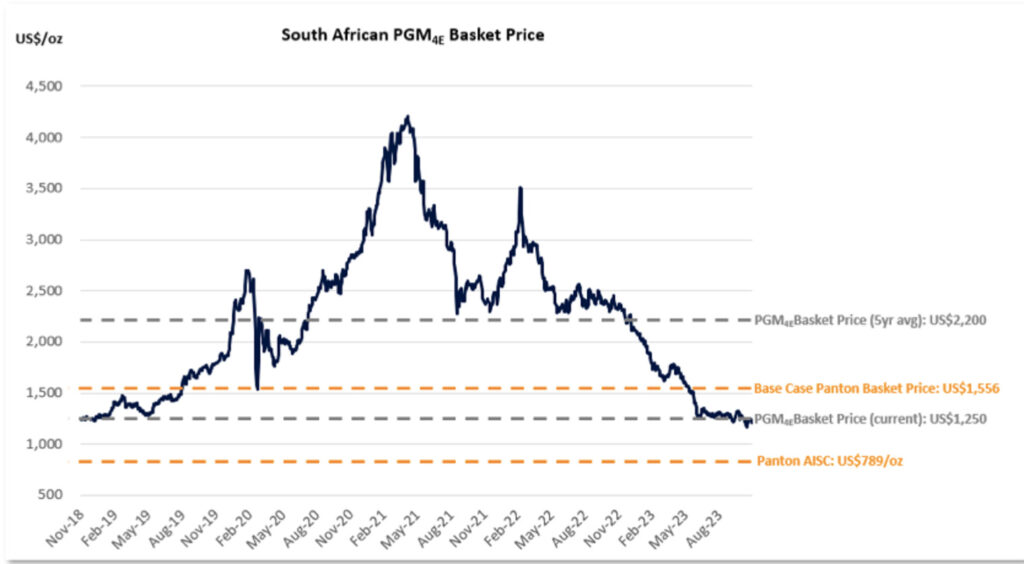

All in sustaining costs of US$789/oz has it down the bottom of the global cost curve, putting FME in a strong position to ride out any price weakness.

And as one of the only near-term development prospects for PGM supply outside of Russia and South Africa, Panton places the company in a “tremendous position to grow value through 2024 and beyond,” Future Metals (ASX:FME) MD Jardee Kininmonth says.

“Future Metals’ team has capitalised on the significant bank of prior work completed on the project and its superior grades to develop a conventional flow sheet producing saleable PGM and chromite concentrates at a meaningful scale in a global context,” he said.

Robust economics and basket price

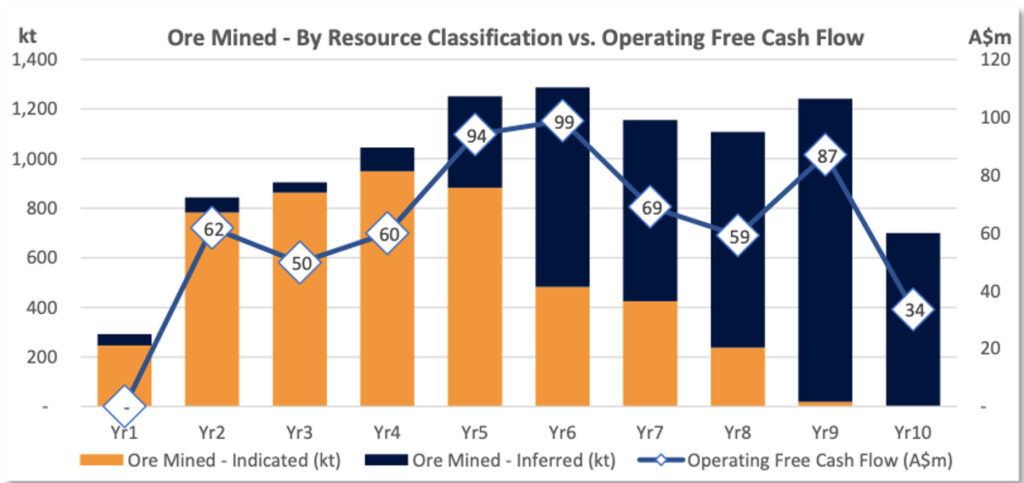

The study’s robust economics also reflect the high-grade and low capital intensity of the Panton project, with capex is around A$267m (including a A$32m contingency) and a base case NPV of A$250m (pre-tax), IRR of 26% (pre-tax), operating free cash flow of A$72m per annum and a payback period of just 4.1 years.

Importantly, the estimated AISC (net of by-products) of US$789/oz (projected 2nd quartile) is expected to provide the opportunity for the planned future operations to generate robust operating margins in all phases of the PGM price cycle.

The current PGM 4E (platinum, palladium, rhodium and gold) basket price of ~US$1,250/oz means approximately 35% of existing PGM production globally is loss-making.

This creates potential for a significant amount of supply to cease in the near to medium term unless prices increase.

“We are very pleased that the Panton scoping study demonstrates robust economics for a globally significant PGM-Ni-chromite Project,” Kininmonth said.

“The scoping study shows a robust project which can withstand downturns in the PGM price cycle and provide significant leverage to upswings in prices too.

“The company plans to progress Panton swiftly through the various feasibility stages in order to be as production-ready as possible during the next upswing.“

Mine life extensions through resource growth

The scoping study includes just 26% of reef and high grade dunite material and with an average annual operating free cash flow of A$72m, the value-add of mine life extensions is clear.

FME plans to target this via a progressive uplift in resource categorisation.

The company intends to complete a review of the resource in conjunction with the study mine planning to define the areas which require further drilling to upgrade them from inferred to indicated – and has included $3m per annum from Year 5 for infill drilling costs.

There’s also the potential for additional by-product credits for copper, cobalt, rhodium and iridium along with resource delineation and inclusion of processing feed from nearby projects such as the Eileen Bore project or other discoveries within FME’s 176km2 exploration acreage.

Plus, the study does not include the near-surface bulk dunite mineralisation, a component of the resource which comprises 55.7Mt at 1.2g/t palladium equivalent, and FME says future metallurgical studies may support a significantly expanded operation.

Pre-feasibility study next cab off the rank

The study provides support that Panton is a commercially viable project and accordingly, the company now plans to commence a Pre-Feasibility Study (PFS) to further de-risk the project and finalise a development case.

FME also plans to further optimise the processing flowsheet, undertake metallurgical variability testing, progress offtake discussions and improve the geological confidence of the resource.

Additionally, the company will begin preparing the project for regulatory approvals processes.

FME is targeting completion of the PFS in Q4 2024.

This article was developed in collaboration with Future Metals, a Stockhead advertiser at the time of publishing.

This article does not constitute financial product advice. You should consider obtaining independent advice before making any financial decisions.

The post Future Metals’ low-cost Panton project to generate robust margins in all phases of the PGM price cycle appeared first on Stockhead.